UnitedHealth Group Makes $330,000,000,000 a Year, And You Can Profit Too!

Or lose absolutely everything you have, either way!

So, America. Our Healthcare is in crisis. The reason? It makes way too much money. For the companies that make so much money, it would be insanity to ever walk away. It’s like they were handed dice that only roll 7s. Can’t Stop. Won’t Stop.

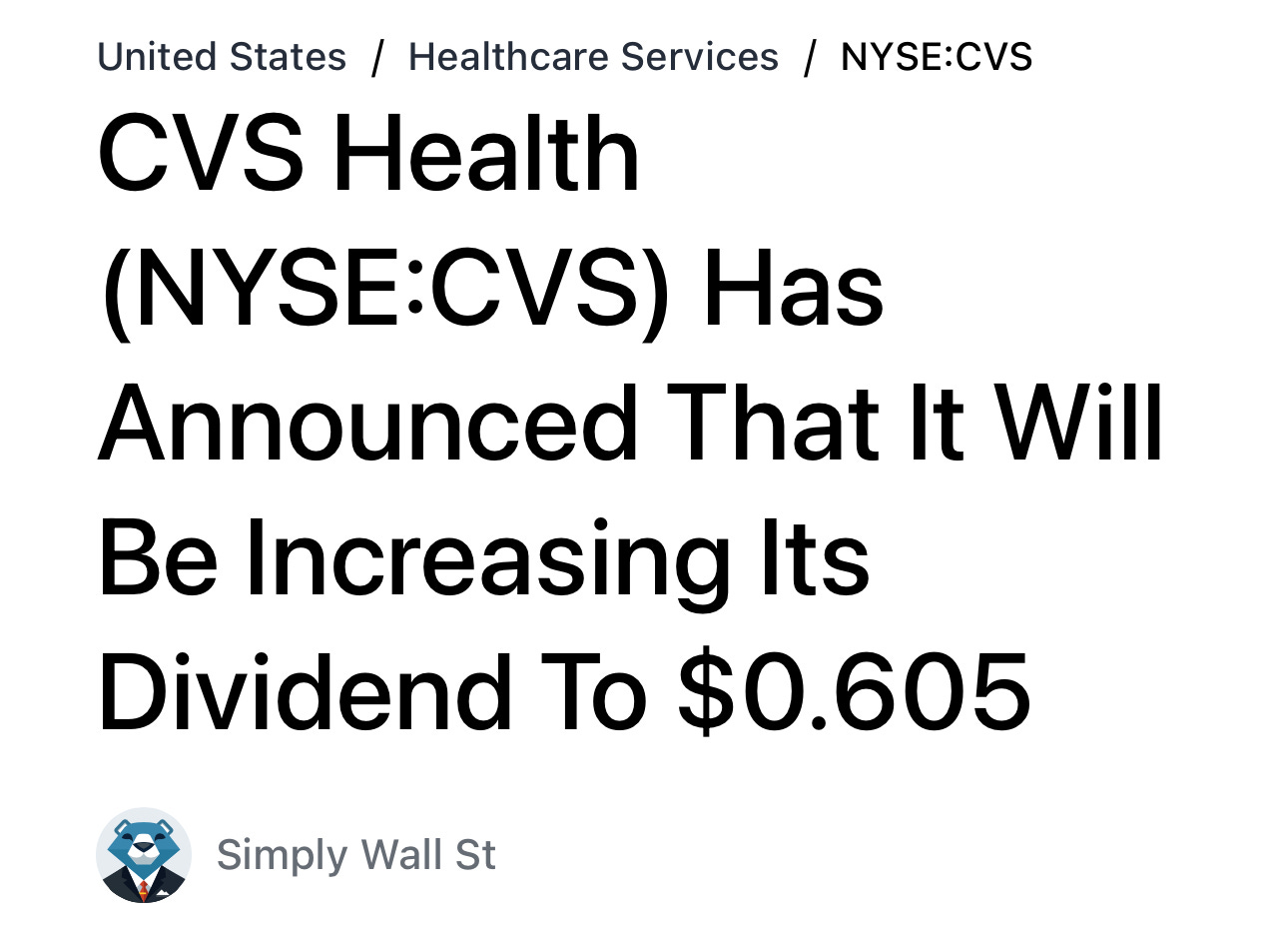

There is a bind. United Healthcare makes $330,000,000,0000 annually. CVS makes so much money they are paying more dividends: YES, in 2023.

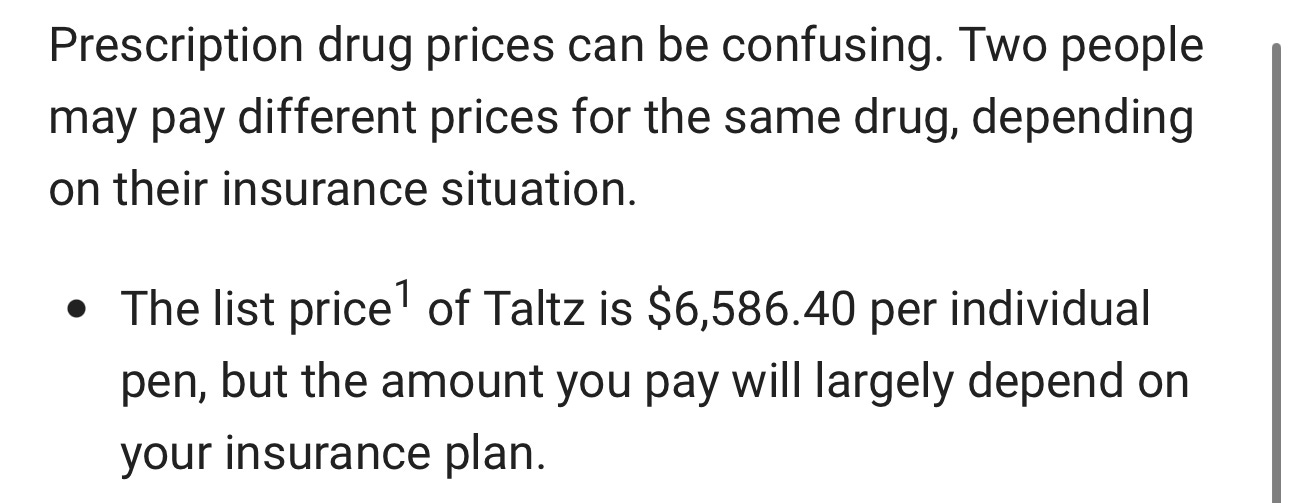

And why do these companies make so much money? Because people are sick, dying, and paying interest on their debts. I have medical debt. You might too. I literally am sicker every day than I need to be—personally— because my insurance (Anthem—Sup!) won’t pay for both Taltz:

Which I have to take monthly, and Xeljanz:

Which I would love to take along with it. I’ll define “love”: My doctor prescribed this combo—as a leading researcher in the field after I have tried and failed to find appropriate relief with (in order of trials):

Methotrexate Plus Cimzia

Cocentyx plus Methotrexate

Twice The Maximum Dose of Cocentyx

And Now Taltz Plus Xeljanz. Except I can’t afford the Xeljanz.

But they are never covered at once. My doctor only has authored 47 Rheumatology papers. He’s a top doctor. But I don't have the cash, and even reimported from abroad it would be another $800/month. And they don’t take credit cards. Only cash.

I also take a GLP-1 medicine, which made me go from having diabetes to not having diabetes1. In under a year. That is another $1000+ a month.

I could go on, but I will just point out that for one human to have a “burn rate” just for meds of more than twice the annual household income? This is not sustainable. For me, or for any employer, plan member, adult, child, duck, dog, or adorable emoji. No one wants that…

Except for the billions and billions made by the drug makers, hospitals, Big Payers, PBMs, General Purchasing Organizations, and other associated entities for whom this is the reason they have their own health insurance coverage…because heaven forbid they have my problems.

The people who work at those companies aren’t bad people. They are decent and well-meaning. They are doing their jobs. They have a fiduciary duty to their investors. They would be violating their duty to their board and investors to blow up their financial model. They are not bad people. They are angels, in many cases. I’m looking at you, everyone who I know in these roles. However, we need to have a frank chat.

I will quote the former head of communications for a major payer Wendell Potter :

To win approval of a $37 billion deal that would reduce competition and make a handful of executives considerably wealthier than they already are, Aetna decided to make life considerably more uncertain for hundreds of thousands of human beings who had been paying good money to Aetna for access to medical care.

We’re not talking about widgets being discarded by a manufacturer. We’re talking about men, women and children, some of whom you might know and, who knows, maybe even care more about than Aetna’s rich executives. People with names, addresses and social security numbers. People who go to church and school and soccer games. People who unfortunately get sick or hurt every now and then and who, in anticipation of that possibility, buy insurance they think will be there when they need it. People who can’t even imagine what it’s like to be paid $27.9 million a year, like Aetna CEO Mark Bertolini was paid in 2015. People, in other words, like you and me.

Brutal—and Wendell was one of them. It is easy to be hopeless. I am not among the hopeless. Here is why: some people, maybe even my readers, will make a metric ton of money betting against this nightmare scenario being sustainable.

I’ve written about automated compliance and how the #AI revolution and novel technology like DoNotPay’s Early Testing will be a vector for a better future. In fact, when I wrote about that topic? My citizen journalism reporting on my personal struggles with illegal healthcare billing and ADA noncompliance2? It was a hit. My daily readership blew up:

And it made people very uncomfortable. But to be very clear, this approach is not just ethical—it’s also very very dangerous and profitable if you can pull it off, as I will imperfectly illustrate.

Step one: look up United Healthcare stock:

And kiss your future goodbye. The good news is that even if the following steps lead to a financial disaster, we are all dead in enough time anyway. And at least you aren’t burning $150k+ a year on life-sustaining medicine…yet.

What follows is the opposite of good financial advice. It is a terrible idea. I have not done this myself. I own 4 whole UHC shares on the opposite hypothesis! Do not under any circumstances bet against United….

Short Sell United Healthcare (or your big health player of choice). To give you a sense…

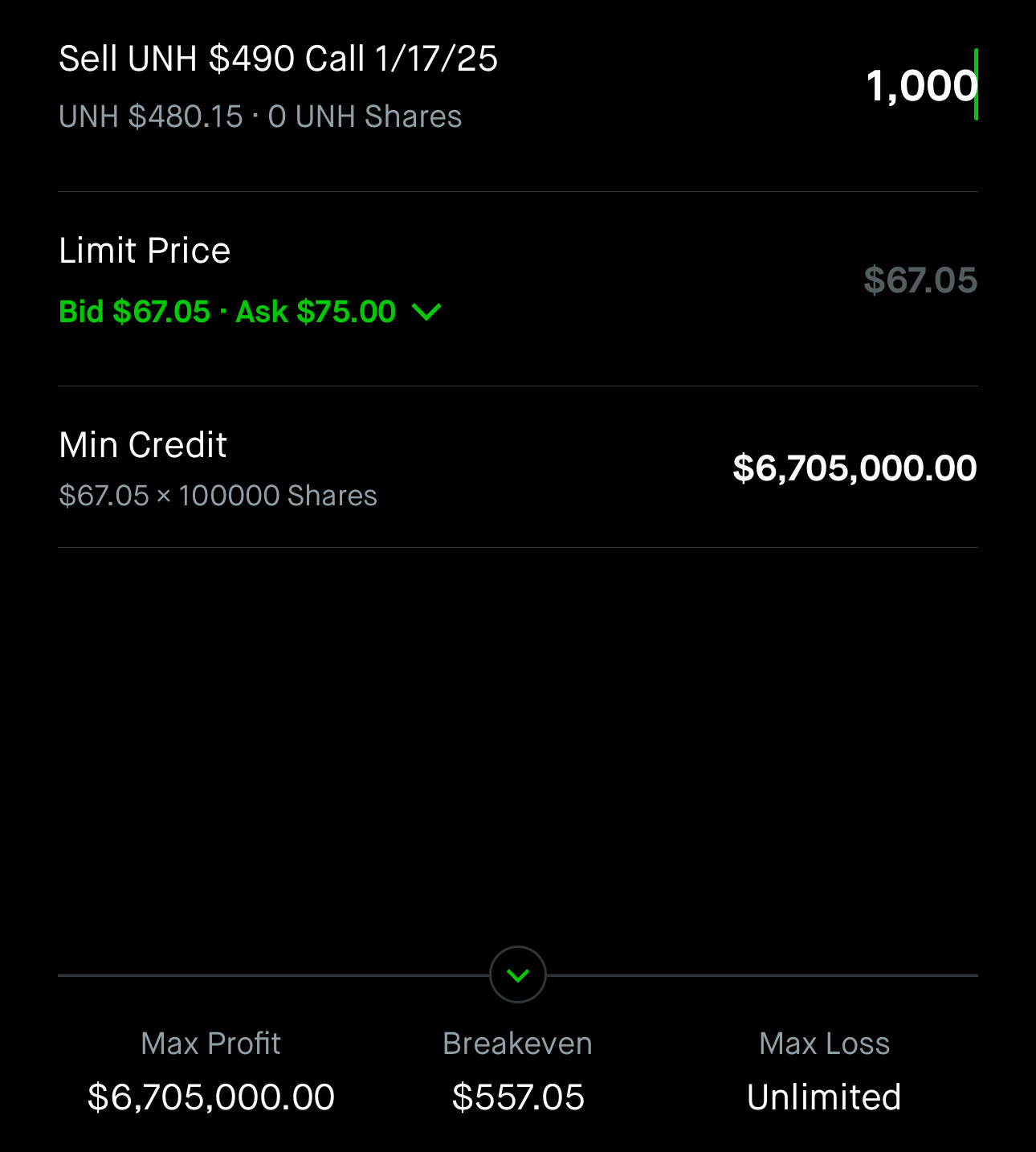

Please, God, do not be willing to bet your future on selling uncovered United call options, which is a financial disaster:

It is inherently risky as there is limited upside profit potential and, in theory, unlimited downside loss potential. In fact, the maximum gain is the premium that the option writer receives upfront, which is usually credited to their account. So, the goal for the writer is to have the option expire worthless.

“Expiring worthless” means United's share price goes down, so the option to buy it at the higher price isn't worth anything to anybody, and you keep money in your pocket. It’s also what all human bodies will do after they generate billing for hospitals and UnitedHealthgroup’s myriad claims processing, analytics, consulting, banking, PBM, and other interests!

Unlimited losses. I will go on to argue that unlimited losses? YOLO.

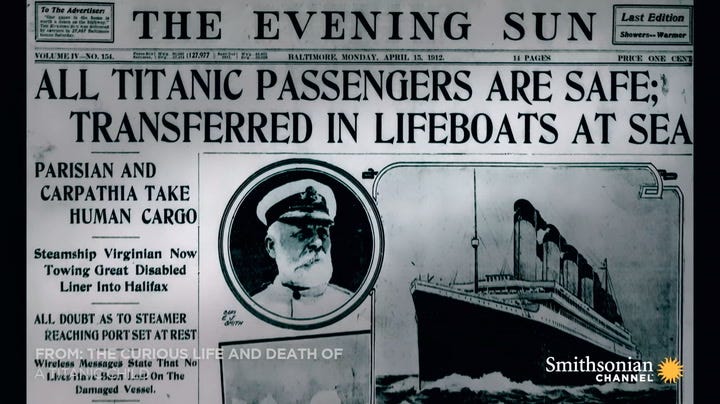

Now, if you were willing to take that bet, the only way to make it pay off…would be to tell the world. Like your life depended on it. “United is a sinking ship! “ Hope all of your friends can abandon UHC and its many tentacles! This is not possible. Do not do this. It’s the Titanic of health plans. It’s too big to fail.

Here are possible ways to desperately attempt to avoid the financial catastrophe that awaits you if you dare to short the stock of a major healthcare company like United:

None of the BIG HEALTH plans have ever been found to be ERISA compliant, and thus any employer purchasing Health Insurance would have a duty to not buy these plans under the CA 2021 Fiduciary Rule. Sue your employer if they buy it.

Get a job at the FTC and aggressively continue to prosecute their anti-PBM agenda.

Send all your friends videos of Eric Bricker and Dr. Glaucomflecken.

Lobby Congress to act on the repeal of the safe harbor rule for PBMs

Build value-based healthcare companies that exist to survive Armageddon.

Short sell harder and buy drug companies, and then drive down the cost of meds

Become a Health Rosetta insurance broker.

Be Mark Cuban and Keep Doing What You Are Doing, You Shark!

Just use the money you made from the short to pay for people’s health care so they don't have to buy UHC Plans?

Accept that you will be insufferable.

Kiss your health tech exit dreams goodbye.

Get great bags for your holiday gifts:

And a billion more things. Become the same kind of pain in the ass everyone was in Brooklyn about Bitcoin circa early 2021, just about this topic. You will become as unpopular at social events as I already am!

Driving down healthcare costs in a way that one can profit from is a business strategy.

It’s also quixotic and impossible.

On the upside, given medical debt math:

23% of Americans have medical debt.

30% of millennials

24% of Generation Xers

22% of Gen Zers

13% of baby boomer's

30% of parents with children younger than 18 have medical debt

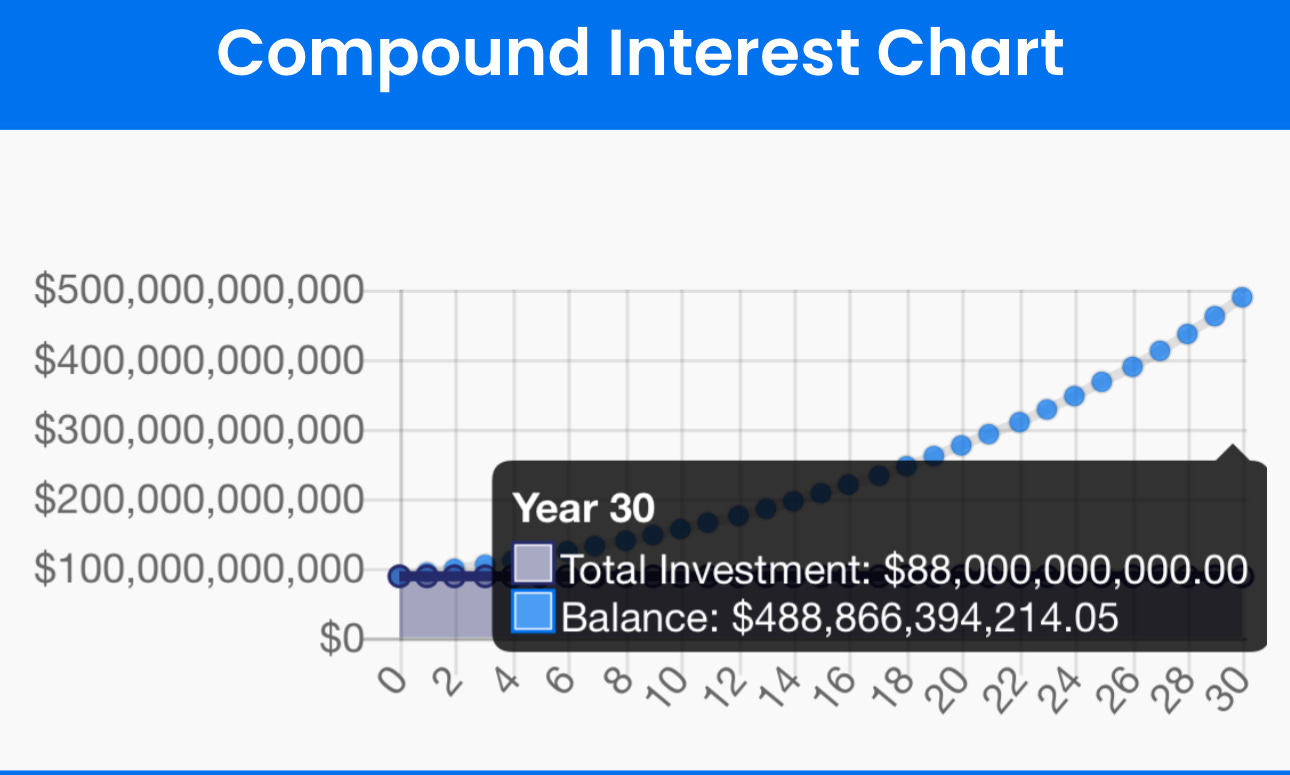

This might be the only rational strategy for all of our future. The $88 billion of current medical debt, assuming it compounds at current interest rates, with no addition to the principal, ends up looking like this in 30 years when millennials inherit the future:

$488 billion in 30 yours is just the compounding interest on what we will owe based on the predatory Big Health financial models that have made UHC so profitable —and made it completely impossible for any reasonable executive at such companies to disagree with their business plan. It would be like the Witch King of the Nazgul walking into Sauron’s office and trying to make the case that “it’s really time we drop this one-ring obsession and pivot to an orc wellness model.” That wouldn’t be in keeping with Mordor’s core values, and before you know it, someone is a bad cultural fit.

But you know what, as long as you have your health…right?

For nerds, My HbA1c went from 7.4 to 5.2

Mount Sinai got back to me. They insist their website is ADA-compliant. I helpfully informed them that this was an automated complaint and that I really just want them to know automated complaints are coming. They had no answer for why they were 501r non-compliant. Their legal council didn’t seem to know what that was. They didn’t respond to that compliance issue in a timely manner. Whatever, It’s not like I emailed their compliance department about it. And it’s not like their tax-exempt status is on the line. And it is not like this article and all the others are documentation of that potential compliance issue, and in a very “white hat” move, I made them aware of the issue. The non-response and all those emails and even this article is a discoverable paper train in an audit. They should be fine. I’m not going to be the one coming after a hospital. But once a compliance issue hits a compliance inbox, it’s probably a good idea to address it.

I was recently prescribed Dupixent for long-Covid-related exacerbated asthma which put me in the hospital for 8 days in mid-March. Copay for Dupixent from my Humana Medicare Advantage plan? $1600 every two weeks! Now checking with pulmonologist if I can walk the tightrope to see if my pulmonary symptoms since I had Covid in May (pneumonia x2, one with an overnight ER visit, once with a 5-day hospitalization; bronchitis x3; 10 weeks of recurring episodes of asthma with intermittent 12-day treatments, then taper with oral Prednisone; latest hospitalization began with a 911 call when my pulse ox dipped below 85; so much IV steroids in latest hospitalization that I had benign visual hallucinations) are gone for good, or if I have to go on the begging circuit with Humana and with the manufacturer of Dupixent. Simply put, the system sucks.