Can’t Find a Psychiatrist Who Will See You in Network? Now, You Can Sue Your Company!

Legal updates mean the legal threat is increasing for employers.

The Frontier Psychiatrists is a daily health-related newsletter. It has a humorous tone about serious issues. Owen Muir, M.D., writes most of it. Today—because it’s a lazy Saturday—we feature light reading about health insurance and compliance standards under ERISA!

Guess what? Chicken butt. Guess why? Because there’s a regulatory compliance enforcement opportunity or disaster, depending on your perspective. Also, chicken thigh.1

Do you know health insurance comes out of your paycheck before taxes? If you do have a job and it offers health benefits, you have the option of health insurance.2

It turns out that for employer-provided health insurance in the U.S. if your employer has to comply with ERISA3, they have significant liability. As of 2021, Fiduciary Duty was definitively added to the Combined Appropriations Act.

What’s a fiduciary? A fiduciary is someone who has to act in your best interest. This is defined financially. Your benefits can’t provide coverage below minimum legal standards when paying for health benefits. The audit standards are laid out by the Department of Labor, which is helpfully accessible here.

Compliance with these laws is what makes health insurance pre-tax. It’s employment law. It’s tax law. It’s both. It’s the Pizza Hut and Taco Bell of legal statutes in the same convenient place!

The health insurance business is good to be in…for payers:

And great for their CEOs:

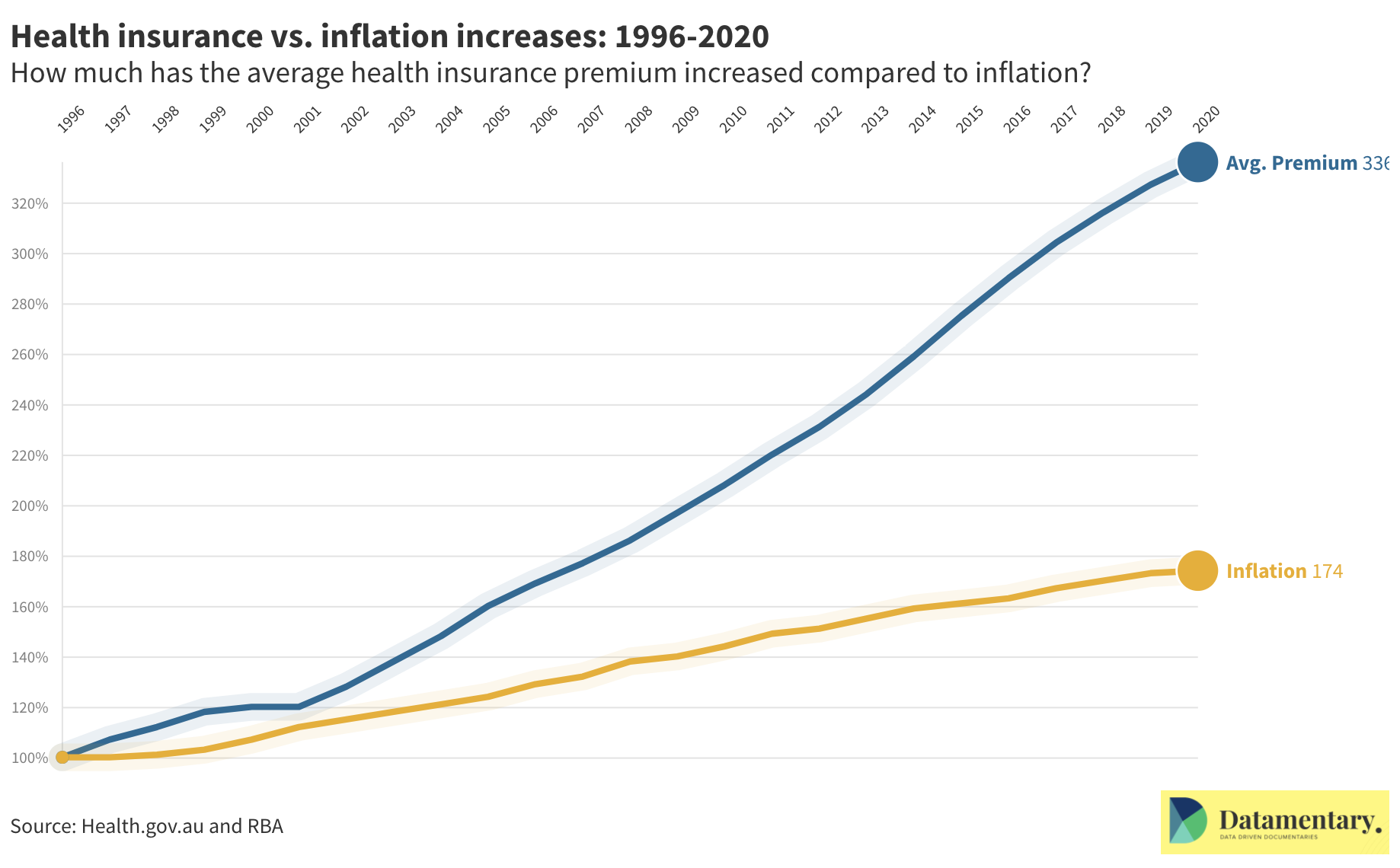

For consumers paying premiums, it is less of a stellar arrangement; they are going up!

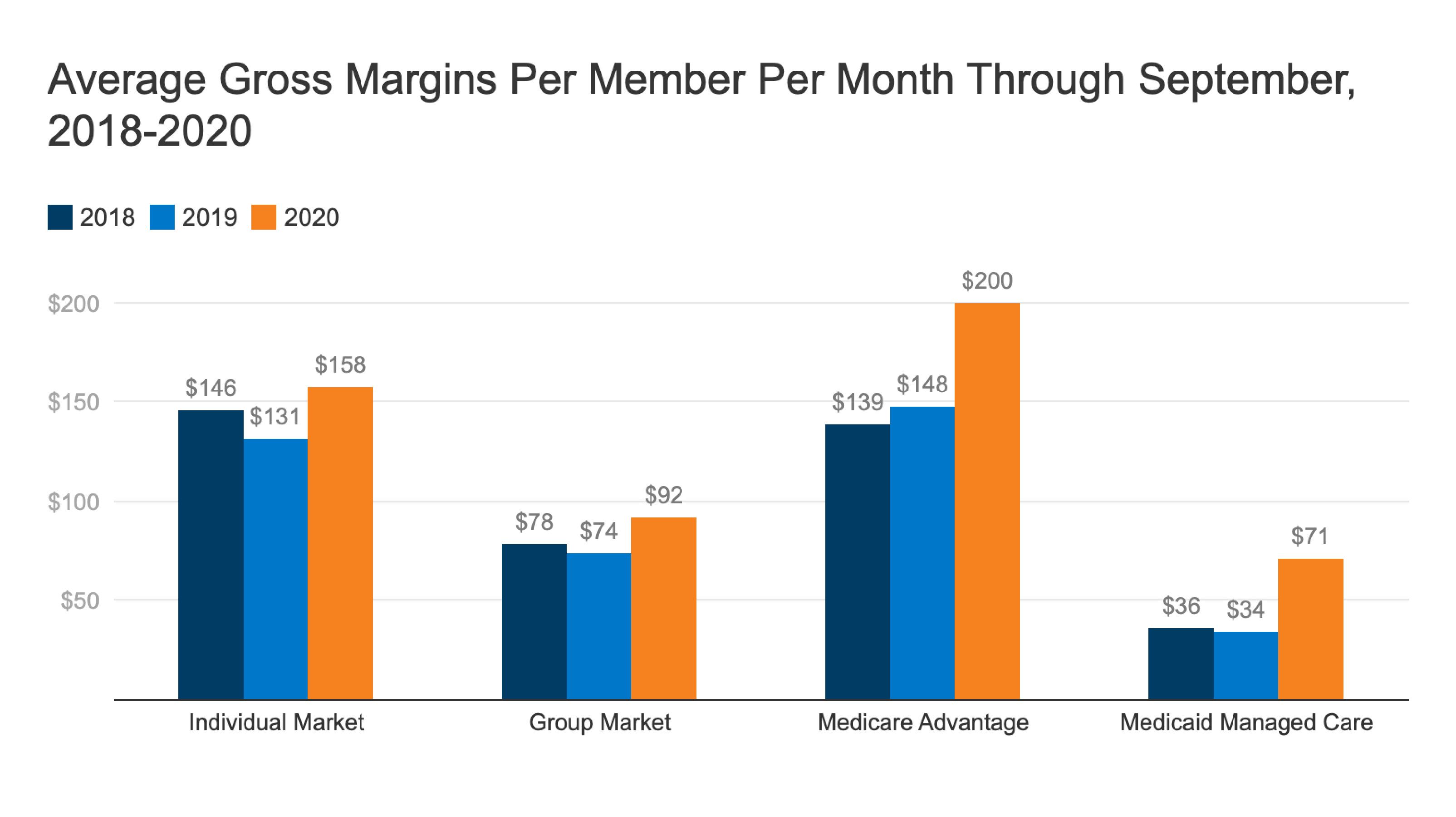

For a long time, brokers could legally accept payments and didn’t have to disclose them to employers. This makes for a very cozy golf game. You want someone to have a fiduciary role because there are known penalties if they scam you. It’s not hard to compare the very, very different gross margins across plan types to see profits are not evenly distributed:

It wasn’t, technically speaking, legal to scam employers; enforcement was absent, however. Taking undisclosed payments is not even legal when it comes to getting songs played on the radio. Except it was, sort of, in healthcare.

So in 2021, it was made entirely, obviously, officially illegal for employers, and the brokers they buy insurance from, to engage in non-fiduciary behavior.

The duty, it should be noted, is to the plan member. A.k.a., the person who has the insurance coverage. A.k.a., almost all of us, from our jobs.

This has a practical upshot for every single one of us who has employer-provided health insurance under ERISA.4

We have a right for that coverage to be in our best interest.

That has some precise definitions. Some of them are highly actionable by individuals without having to be legal scholars.

Obvious things you can win a fight about:

Under the accountable care act, there are rules about network sufficiency. This means all insurance by private employers covered under ERISA must meet minimum standards.

The most obvious minimum? It is the time it takes to get an appointment.

And the maximum waiting time for a mental health appointment… is…up to…

Ten days.

For any outpatient appointment. For any condition.

So let’s use an undeniable and easy-to-prove example: let’s say you live in the state of Texas, Florida, Utah, Arkansas, etc.

Let’s say you have a child with gender dysphoria.

In states with bans on gender-affirming care, the wait time for an appointment for your child’s gender dysphoria, assessment, or treatment, is now infinite5.

Now let us imagine you’re looking for transcranial magnetic stimulation for your treatment-resistant obsessive-compulsive disorder. Imagine you have health insurance other than one run by the wise administrators at Evernorth (a.k.a. CIGNA).

There is only one FDA-cleared treatment for treatment-resistant obsessive-compulsive disorder. It’s TMS (Ideally with the Brainsway H7 coil). If you have almost all Big Payer plans, you have an employer that has purchased health insurance that never pays for the treatment—it’s a plan exclusion!

That is, conceivably, a breach of fiduciary duty to you— because you have a right to mental health parity in your health insurance. If there’s an FDA-approved treatment that your insurance will never cover, you have the right to sue your employer for buying insurance that doesn’t cover the thing. It’s an open question if subsequent legal action can also recoup damages related to delays in treatment.

The Covering Of @&$ Begins.

Your employer needs to get compliant. And they’re probably going to call their Benefits Broker. It is in the interests of those parties to file suit to cover their own liability, too.

At a bare minimum, they’re probably going to want to buy a compliant plan during the next enrollment cycle. Who the heck would want to stand in the way of that particular wrecking ball? Or go to a self-funded plan where they can make sure they're compliant using a tool like the Health Rosetta Plan Grader.

Now, those are obvious cases. If you think your benefits suck, from a regulatory standpoint, that’s probably true.

And if ERISA wasn’t bad enough, I suspect Perez v. Sturgis will be applied for damages under ADA next. Health Plans— the new Lawyer Employment Act of 2023!

I was planning to offer my readers the opportunity to buckle up. On compliance audit, it looks like we're all out of buckles, given the number of regulatory updates recently!

You can still…

I have seven-year-old children who enjoy this kind of humor.

Depending on the size of your employer, blah blah blah. This stuff is boring. Let’s not pretend otherwise.

It doesn’t apply to people who work for the government.

this excludes government employees and some other groups.

Or, at the very least, until Governor Gregory Abbott is run out of town on a rail. Because when he defined gender-affirming care as child abuse, he assured that people would not put themselves at risk of documenting accurately, and so there probably are no available gender-affirming care visits in the state of Texas. And, whether you like it or not, that’s a condition listed in the DSM 5. So it falls under a behavioral health appointment according to the ACA, and your health plan is legally only allowed to make you wait ten days for an appointment.